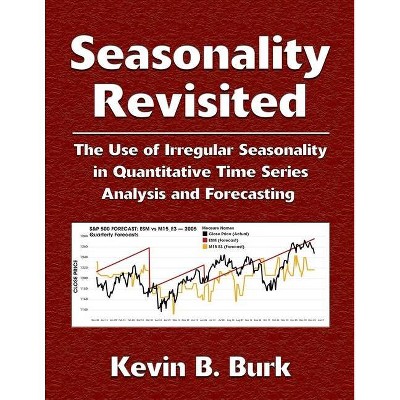

Seasonality Revisited - by Kevin B Burk (Paperback)

Similar Products

Products of same category from the store

All

Product info

<p/><br></br><p><b> Book Synopsis </b></p></br></br>Seasonality RevisitedThe Use of Irregular Seasonality in Quantitative Time Series Analysis and Forecasting<p>This monograph revisits the theory of seasonality by asserting that seasonality is a quality of time, and that the calendar and the clock are not the only ways to measure time. Every season has an effect that can be quantified using Cohen's d, which makes it possible to compare seasonal effects between different seasonal models. The historic variance of the effect sizes can be used to determine the predictive value of an individual season for that data set.</p><p> Irregular seasonal models, derived from the cycles of the planet Mercury, are compared to regular seasonal models using Calendar Month seasonality as the baseline reference of significance. </p><p> The quantified significance of Calendar Month seasonality is used as the baseline of comparison to evaluate the potential significance of the irregular Mercury-based seasonal models. The seasonal models are compared across three extensive and unrelated data sets: Transportation On-Time Performance, Car Crash, and Financial Market data. The Mercury-based irregular seasonal models showed a far greater percentage of significant seasons than the Calendar Month model. The ability to compare and contrast seasonal effects in this way demonstrates the practical value of the effect- and variance-based approach to quantifying seasonal influences. It also confirms that irregular seasonal models can reveal patterns in time series data that are otherwise undetectable. </p><p> To test the value of incorporating irregular seasonal influences in time series forecasting, 76 quarterly forecasts covering a 19-year period from 2000-2018 were generated for each of <strong>430 individual financial data sets </strong>(10 stock market indexes, 379 individual stocks, 21 commodities, 10 interest rates and bonds, and 10 currency exchange rates). The aggregate accuracy of twelve different forecast models was then ranked and compared with both mean absolute percentage error (MAPE) and root mean square error (RMSE) The forecast models include five non-seasonal traditional forecast models (ARIMA, ESM, HOLT, MEAN, and NAÏVE), the seasonal forecast generated using the M15 Sign + Speed seasons, and six hybrid seasonal forecasts that combine the seasonal forecast data with the forecast data of each of the traditional forecast models. </p><p> Two different methods, designated, E3 and M3, were used to generate the seasonal forecasts for the entire data set. For the forecasts that used the E3 model, <strong>the hybrid seasonal forecasts were more accurate than their non-seasonal counterparts 71.30% of the time </strong>(MAPE) <strong>and 66.93% of the time </strong>(RMSE). For the forecasts that used the M3 model, <strong>the hybrid seasonal forecasts were more accurate than their non-seasonal counterparts 74.37% of the time </strong>(MAPE) and <strong>72.33% of the time</strong> (RMSE). This clearly demonstrates that including the irregular seasonal influences has a significant chance of improving the accuracy of the forecast. </p><p> The conclusions of this study are that there is clear and consistent value in this new approach to seasonality, both with quantitative time series analysis and with quantitative time series forecasting. These discoveries are worth further serious consideration and exploration. </p><p><br></p>

Price History

Price Archive shows prices from various stores, lets you see history and find the cheapest. There is no actual sale on the website. For all support, inquiry and suggestion messagescommunication@pricearchive.us